Supply is the amount of goods or services that producers are willing and able to sell at each price point at a particular point in time #testanswer

The law of supply

In most cases, there is a positive relationship between the price of a good and the quantity supplied of that good #testanswer

At higher prices, suppliers are willing to produce more as it means they can earn more profit

The relationship between individual and market supply schedules/curve factors

Market Supply Curve

The curve obtained from the horizontal summation of individual supply curves

Individual Supply Curve

A supply curve relating to an individual producer

The effect of changes in price on quantity supplied

Price can have either a contractionary or expansionary effect on the supply curve

This is a movement along the existing supply curve

Expansions are an increase in price

Contractions are a decrease in price

The effect of changes in non-price factors on quantity supplied

This has shift effect on the curve, where quantity produced changes at every price point

Rightward shifts $\rightarrow$ increase in supply

Leftward shift $\rightarrow$ decrease in supply

There are many examples that must be known

Expectations of Producers

This is like expected future prices; expected price changes cause suppliers to alter current supply to take advantage of future prices

Technology

Improvement in technology can reduce production costs, allowing suppliers to produce more at a lower cost

Increase in supply is show as a rightward shift of the supply curve

Prices of other goods

If the price of a related good increases, the supplier can shift production to increase the quantity supplied of the related good

Input prices

Production costs - if the input prices go down, supply can increase

If input prices go up, supply decreases

Government Regulation

Government regulations influence the number of suppliers in the market, which increases or decreases market supply

Government regulations can take the form of

Taxes

Tariffs

Subsidies

Quotas

Example

The car market

Government regulation (luxury car tax) $\rightarrow$ decrease in supply, shifting the supply curve from $S$ to $S_2$ at every price point (this is an ideal #testanswer )

Input prices (steel price increases) $\rightarrow$ decrease in supply

Technology (better manufacturing) $\rightarrow$ increase in supply

Questions

Crude oil prices fell below $$100$ a barrel. This led to unleaded petrol prices to faling $4.6c$

Two non price factors are;

Input prices - the fact that crude oil price decreased directly correlated to unleaded petrol prices

Government regulation - decreasing taxes could increase supply, shifting the curve to the right.

An increase - this would shift the curve to the right, allowing suppliers to produce more supply at the same price point

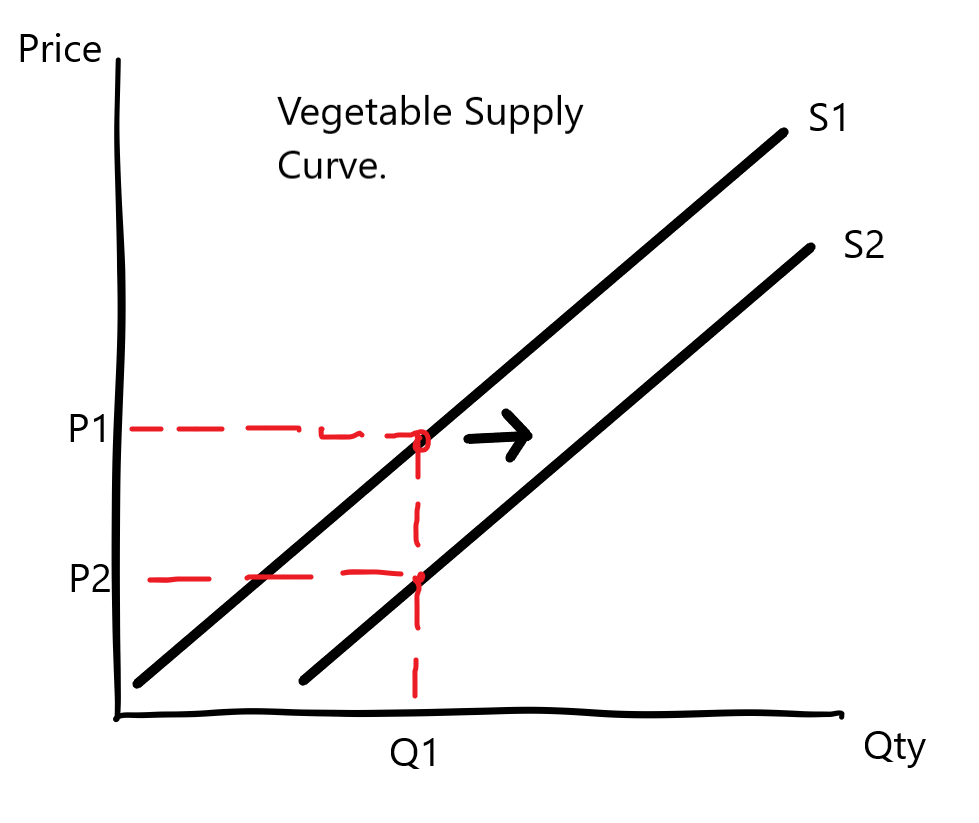

For fresh vegetables, petrol is a massive input price, and therefore a non-price factor. A decrease in such an input price would increase supply in the market and allow vegetables to get cheaper. Below, we can see that at Q1, after the shift to the right due to a change in petrol prices, prices for vegetables decreases.